Behind the Hong Kong Market’s Fast and Mysterious Rally

Global investors are playing a zero-sum game in northern Asia, tussling between Japan, Taiwan and China.

Back in the good books.

Photographer: Paul Yeung/BloombergAll of a sudden, the mood in Hong Kong seems to have shifted. The $5.2 trillion stock market is on its longest winning streak since 2018, with Chinese technology giants Tencent Holdings Ltd. and Alibaba Group Holding Ltd. among the top contributors. Notably, the sharp advance took place in the first few days of May, when mainland bourses were closed for public holidays and Chinese investors were away. It was a clear sign that foreigners were the buyers.

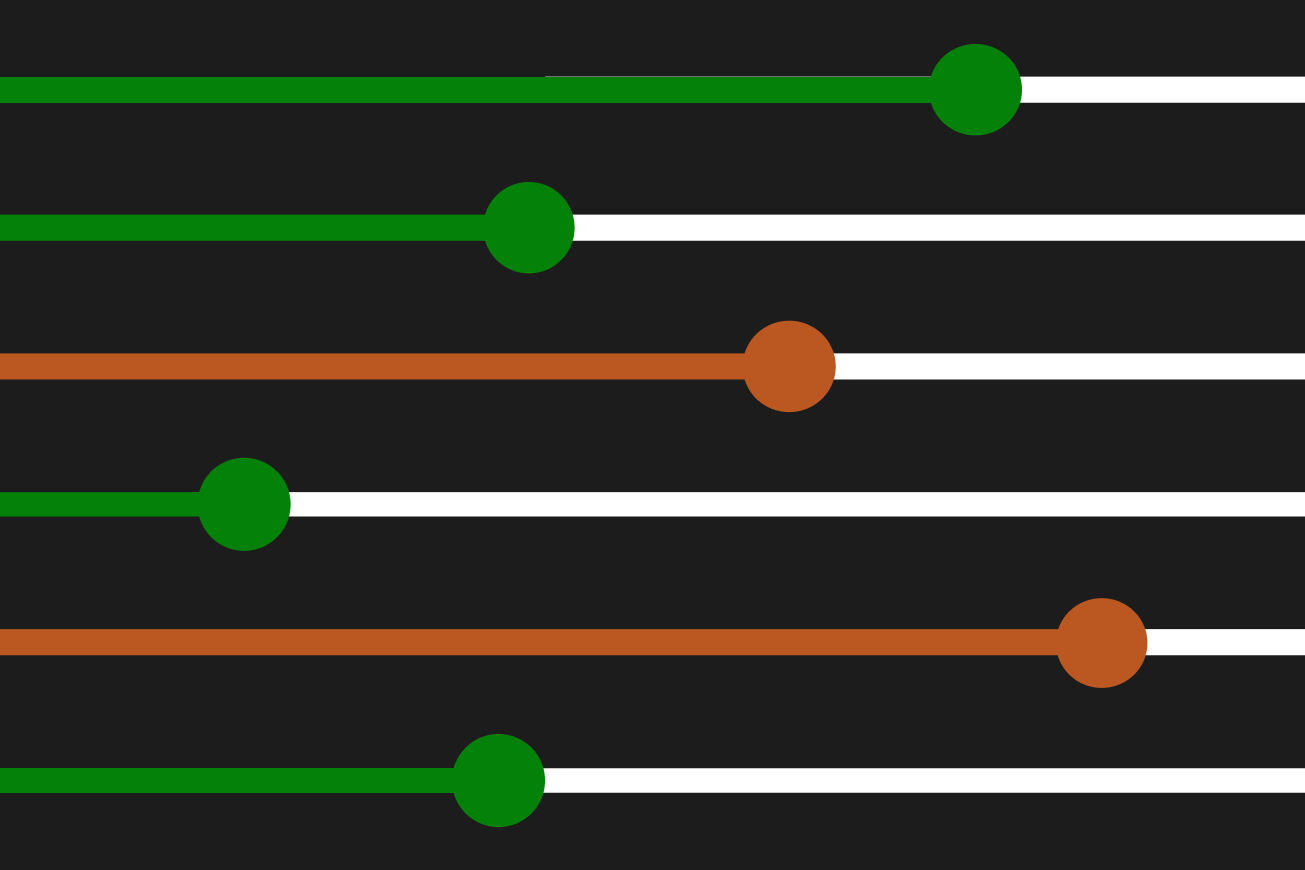

Fast and Furious

Hong Kong's stock market had its longest winning streak since 2018

Source: Bloomberg

Is this bull market for real? It’s a trillion-dollar question.

Two fears — of getting caught and of missing out — are driving this rally.

First, coming into May, investors were heavily exposed to Japan and Taiwan, a chip proxy. They were by far the most-loved markets in Asia, even more than a fast-growing India, according to the latest Bank of America Merrill Lynch fund managers’ survey. Sector-wise, a whopping 60% were net overweight semiconductor companies.

A Crowded Trade

Investors are overwhelmingly exposed to Japan and Taiwan

Source: Bank of America Merrill Lynch

But as the earnings season unfolded and Japan’s golden week holiday approached, asset managers started having second thoughts. Taiwan Semiconductor Manufacturing Co. on April 18 cast doubt over investors’ bullish view that big tech’s AI infrastructure spending alone could propel a chip upcycle. During its earnings call, TSMC, the world’s largest maker of advanced chips, scaled back its outlook, citing weak smartphone and personal-computing demand. Foreign money promptly fled Taipei.

The Imbalance

Investors piled into chip stocks while shunning real estate developers

Source: Bank of America Merrill Lynch

That yen’s slide past 160 on April 29 was also a shocker. It eroded dollar-based investors’ total returns. While the Nikkei 225 has gained about 14% this year, the US-listed iShares MSCI Japan ETF returned only 8%. Even though the Bank of Japan has intervened since, Tokyo’s intensified battle to shore up its currency turned out expensive and the yen remains under pressure amid hedge fund short bets.

At the same time, unloved Chinese assets got a rare boost from Beijing. There’s now hope that the government’s policy paralysis is finally behind us.

Investors were encouraged by the latest readout from the 24-man Politburo meeting, released on April 30. The top policymakers seemed open to taking a different approach to resolving the property crisis, calling for coordinated measures to digest existing housing stock. The last time inventory was mentioned by the Politburo was in mid-2016. A massive stimulus in the form of shantytown redevelopment, a poverty alleviation program that replaced older, rundown dwellings with new, affordable housing, was still in the early stages. The People’s Bank of China unleashed more than 3 trillion yuan ($416 billion) in pledged lending in support of the program and pulled China’s stock market out of a 2015 slump. Beijing has been floating the idea of urban village renovation, or refurbishing rundown areas, over the last year.

The Politburo also addressed the other big policy disappointment — the lack of follow-through on fiscal stimulus. The pace of government bond sales, a major source of infrastructure spending, has been unusually slow this year. “We should avoid slacking off,” the top politicians warned.

We’ve been seeing real money — from less speculative asset managers such as mutual funds — buying Hong Kong-listed shares, according to conversations I’ve had with multiple brokers on trading desks in the city. Buying is most concentrated in large-cap blue-chips, such as AIA Group Ltd., Meituan and Tencent, as these global long-only funds rush to get on the China wagon and thus focus on the most-liquid names. As of March, they allocated only 5% of their portfolios to China, down from 15% at the 2021 peak, data from EPFR show.

Right now, there’s a zero-sum game being played out in northern Asia. Earlier in the year, Japan, Taiwan, and to a lesser extent South Korea, benefited from the pervasive bearish sentiment toward China and thus Hong Kong-listed stocks. Tourist dollars crowded into Tokyo and portfolio allocation became overwhelmingly lopsided and concentrated. Now, many are scrambling to rebalance.

This geographical diversification is likely to stay. After all, just like China, Japan also has a track record of disappointing investors, chip cycles are notoriously volatile, and Beijing has a history of shock and awe. The China trade is back on.

More From Bloomberg Opinion:

- Yen Is Currency Traders' Best Friend and Worst Enemy: Shuli Ren

- Inside TSMC Chairman Liu's Short But Impactful Reign: Tim Culpan

- Japan Is Quiet About the Yen Because It Has to Be: John Authers

Want more Bloomberg Opinion? OPIN <GO>. Or you can subscribe to our daily newsletter.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.